Germany’s CEOs are turning more cautious on investment in 2026

The latest earnings-call–based 12‑month‑ahead CapEx expectations show a clear end‑of‑year drop in Germany.

What the three figures tell me:

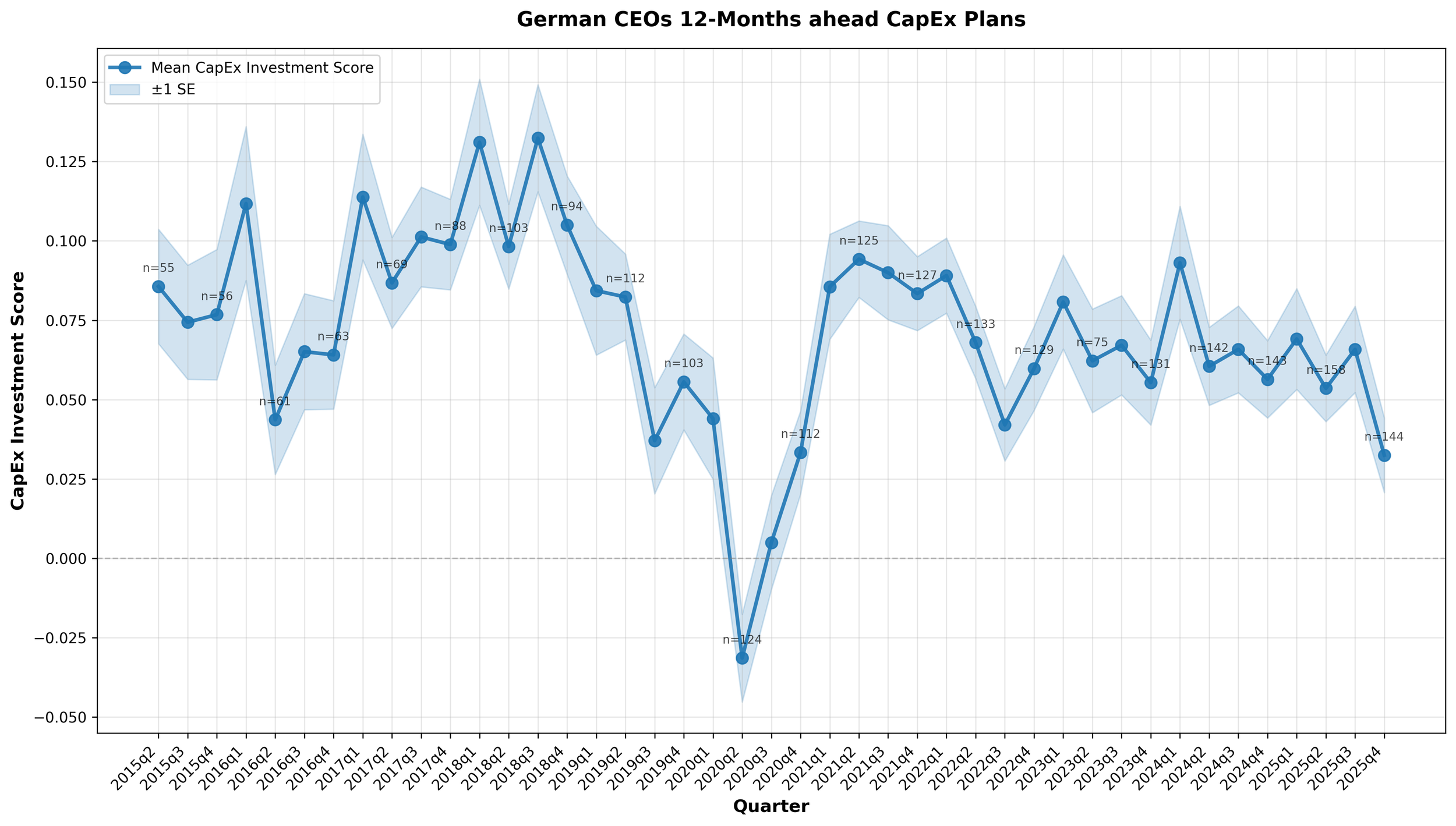

1) Aggregate (Figure 1):

After a relatively stable range through most of 2024/25, the mean CapEx expectation drops sharply in 2025Q4 — roughly a “half‑step down” in confidence — and the lowest level since 2020Q4. We are still (slightly) above zero, but the direction is unmistakable: boards are getting more hesitant.

Figure 1. Aggregate CapEx Investment Score (Source: CfET)

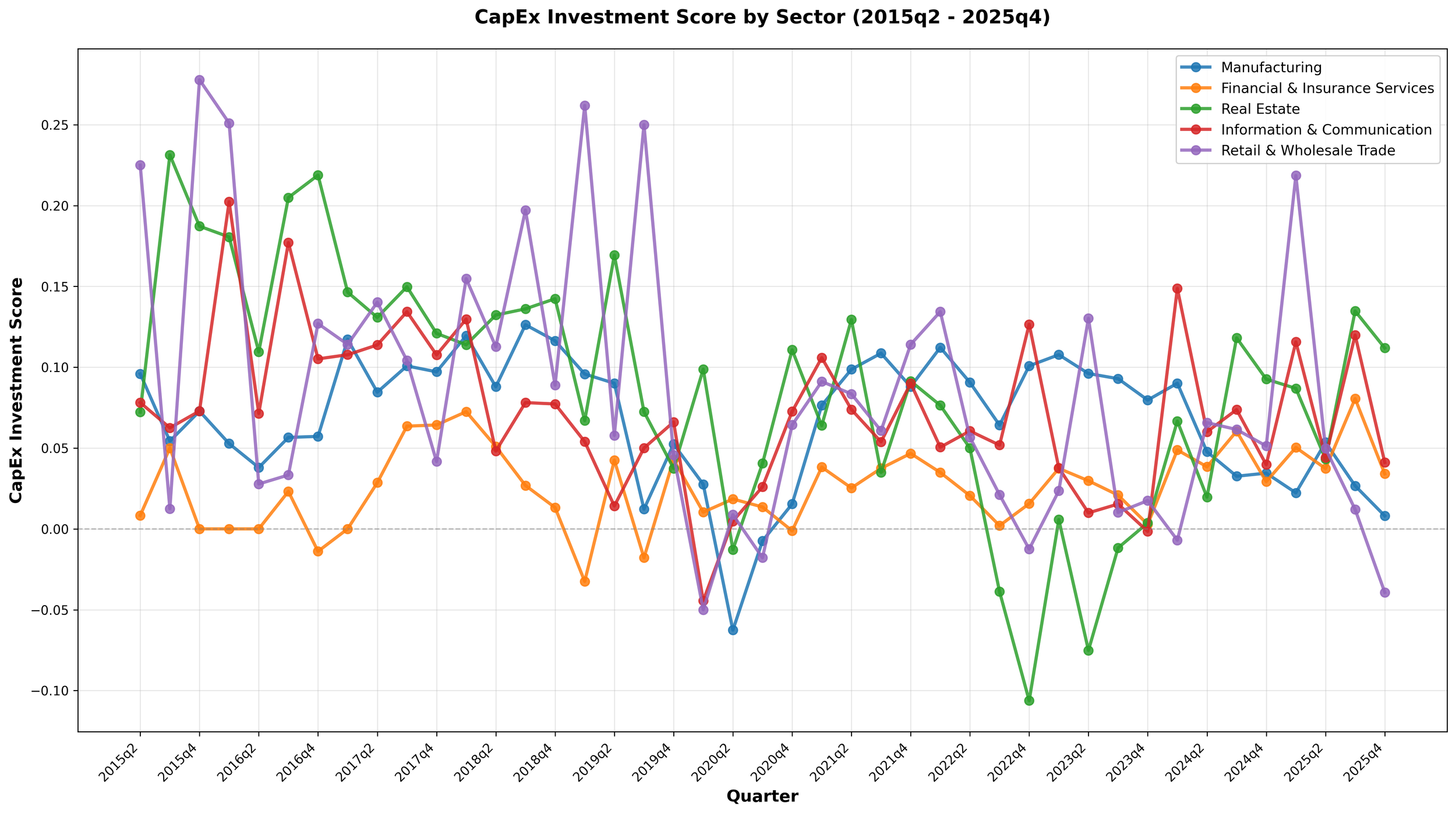

2) Sector split (Figure 2):

This is not a uniform slowdown. The weakness is concentrated where it matters most for the real economy:

Manufacturing: expectations grind down toward near‑neutral.

Retail/Wholesale: turns decisively negative at the end of the year (high volatility, but the latest point is a clear warning sign).

Real estate: rebounds strongly (after a deep trough earlier), showing that the investment cycle is not one‑size‑fits‑all.

Financials / I&C: more stable or episodic — not the main driver of the aggregate drop.

Figure 2. CapEx Investment Score by Sector (Source: CfET)

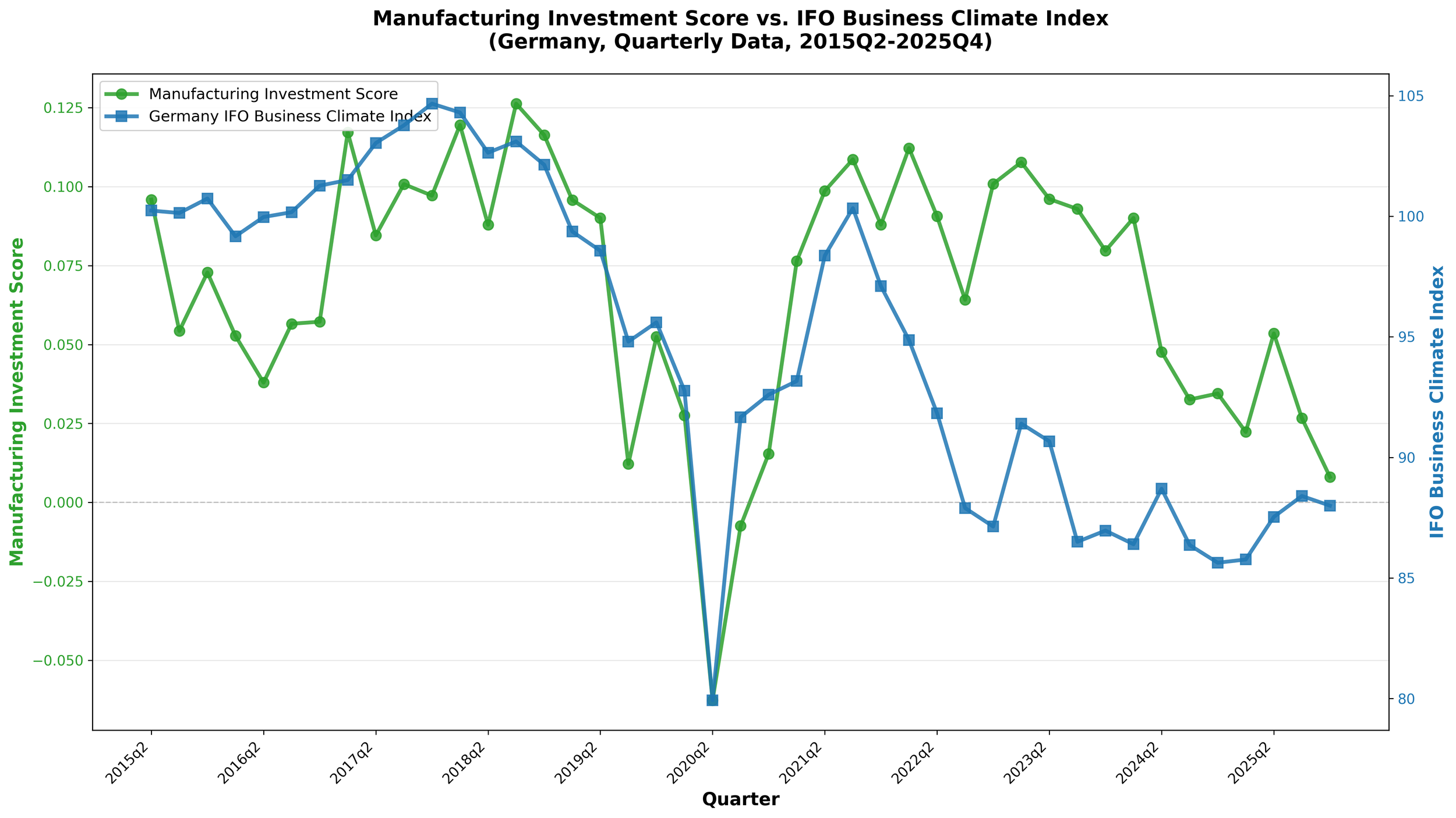

3) Manufacturing vs. IFO (Figure 3):

Manufacturing investment expectations broadly move with Germany’s business climate (correlation about 0.6) and the message is consistent: weak sentiment → delayed investment. What is striking is that CapEx expectations soften again even while the macro backdrop feels “stuck” rather than collapsing.

Figure 3: Manufacturing CapEx Investment Score vs IfO Business Climate Index

The uncomfortable contrast: public ambition vs. private caution

Berlin is putting forward large-scale public investment plans (infrastructure modernization, climate neutrality projects, digitalisation, etc.). That is the right direction. But these charts tell us something important:

Public money alone will not deliver Europe’s transformation if private CapEx is being postponed.

So the real question for Germany (and for Europe) is: How do we turn public investment plans into crowding-in of private investment?

My hypothesis (and what we are testing next at CfET): The “uncertainty tax” has become structural — political risk, climate transition risk, and technology (AI) risk increasingly shape the timing of investment. That is why we are now combining CapEx expectations with earnings-call–based risk exposure measures to identify which risks are holding back which sectors.

If we want a competitiveness comeback, we need:

faster permitting and execution capacity,

stable, credible policy paths (not quarterly surprises),

and financing structures that reduce downside risk so boards can invest.

What are you seeing in your sector — are CapEx committees getting more cautious going into 2026?

If you want to get in touch and discuss this and other data points, please reach out!