The future is hybrid

The debate "Banks vs. Private Credit" is the wrong framing. Look at how European private credit actually originates deals today, and where the growth is.

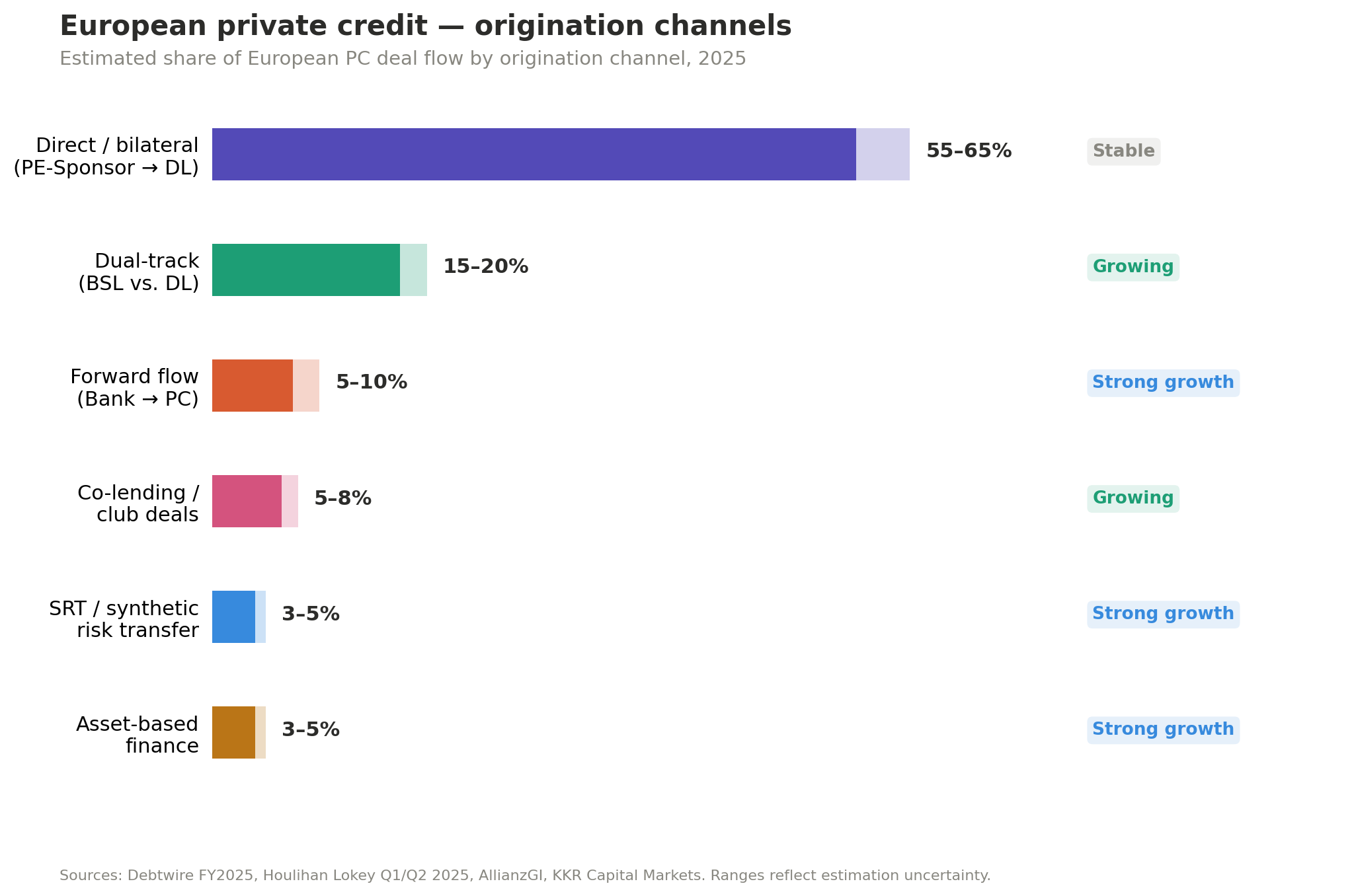

European private credit dealsourcing

Yes, direct lending via PE sponsors still dominates (55–65% of deal flow). That is not changing anytime soon.

But the fastest-growing channels tell a different story: forward flow agreements, where banks originate and private credit funds take the risk. Synthetic risk transfer, where banks keep the loans but offload exposure. Asset-based finance, where nonbanks hold just 13% in Europe vs. 34% in the US.

Every single high-growth channel is a bank-PC partnership, not a substitution.

Three things are happening simultaneously:

1. Direct lending is pushing into upper mid-market territory (€500M+ deals).

2. Banks are becoming origination platforms for private capital.

2. And ABF is the largest untapped opportunity, a €4.2 trillion European market where nonbank penetration has barely started.

The winners will not be banks or private credit funds. They will be the partnerships that combine bank origination networks with private capital's balance sheet flexibility. Securitization is the connection.

Europe does not need to copy the US model. It needs to build its own, starting from its banking relationships, not against them.

What is your experience, where do you see the largest growth? And, what am I missing in this context? (Figure is based on public sources and estimates, let me know if you have better/more precise data and estimates) Discuss below in the comment section. 👇

#privatecredit

#banks

#origination

#risktransfer