The Banks Are Fine. That's the Problem.

Sascha Steffen · April 12, 2026

On Friday, the Federal Reserve began asking major US banks for details about their exposure to private credit. The same week, FSB Chair Andrew Bailey warned that the Iran war is compounding private credit stress. The ECB launched fresh checks on supervised banks' dealings with direct lenders in March. BaFin, ASIC, and Japan's FSA have all initiated data collection exercises in recent weeks. Six regulators, one question: will private credit stress infect the banking system?

The answer is no. And that should worry us.

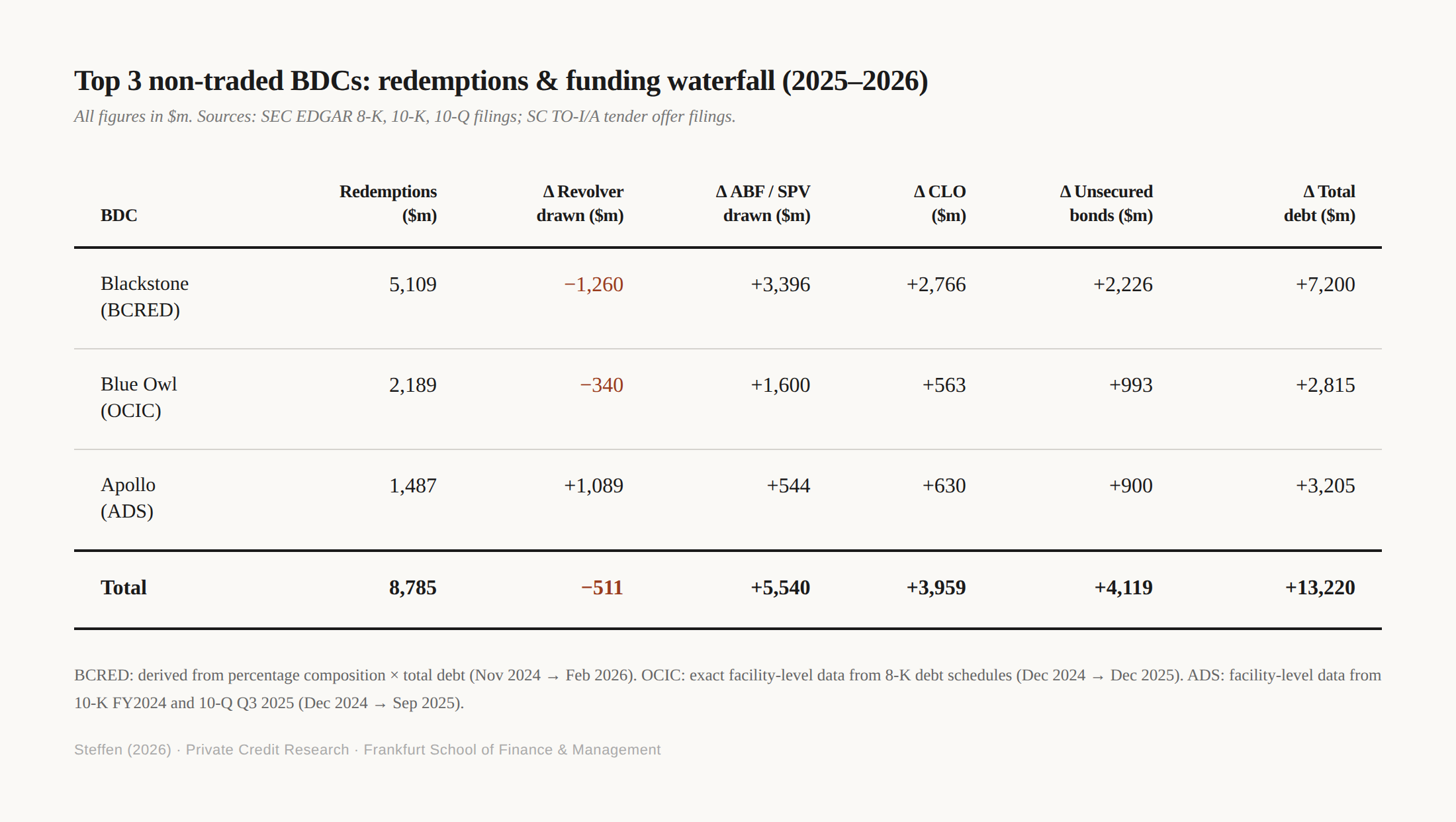

I traced the funding structure for the three largest non-traded BDCs — Blackstone's BCRED, Blue Owl's OCIC, and Apollo's ADS — through their SEC filings over the past twelve months. Together these three vehicles processed $8.8 billion in share repurchases, the majority of redemptions that have dominated headlines since January (in fact, 10 BDCs account for >90% of all redemptions). The question I wanted to answer is very simple: where did the money come from?

Source: Own calculations from official filings

My first key result: Not from bank credit lines, at least not in aggregate. BCRED and OCIC paid down $1.6 billion on their corporate revolvers while simultaneously facing the largest redemption queues in the industry. Apollo's ADS, by contrast, drew $1.1 billion on its revolver, along a rapid CLO issuance and SPV expansion, suggesting the revolver functioned as bridge financing during its build-out phase. The net effect across the three funds: revolvers declined by roughly $500 million.

Out of the 10 BDCs with >90% of all redemptions, only 3 reported an increase in credit line borrowing (ADS, Goldman Sachs' GSPC, and modestly Oaktree's OSCF), and in each case the draws coincided with rapid facility expansion elsewhere in the capital structure.

The replacement funding came from approximately $5.5 billion in expanded asset-backed SPV facilities, $4 billion in CLO securitisations, and $4.1 billion in unsecured bond issuance. Total debt across the three funds grew by roughly $13.2 billion, exceeding redemptions by $4.4 billion. The excess funded portfolio expansion, not liquidity.

These BDCs are not shrinking. They are restructuring their liabilities from short-dated bank debt into long-dated capital markets funding. A key reason is the "borrowing base", a contractually designed re-evaluation of the BDC and its portfolio that serves as collateral to bank credit line lending. These borrowing bases frequently trigger credit line repayment or a reduction in borrowing capacity when redemptions increase.

Moreover, it appears that the weighted average cost of funding has decreased, not increased after the liability restructuring. After stripping out the roughly 65 basis point decline in SOFR over the period, the spread component of blended funding costs still fell by 15 to 50 basis points across the three funds. That is, capital markets instruments are, on average, cheaper on a spread basis than the revolvers they replaced; CLO AAA tranches price at SOFR plus 130–167 basis points, and swapped unsecured bonds at roughly SOFR plus 100–150 basis points, both below the typical revolver margin of SOFR plus 175–200 basis points. While redemptions might have triggered some liability restructuring, it does not look like a forced switch into expensive emergency financing. It seems like a rational cost optimisation that redemption pressure accelerated (but did not cause).

The supervisory implications are direct. Every regulator currently querying bank balance sheets for private credit exposure will find that exposure has contracted since year-end. JPMorgan's markdown of software collateral in March was the event that triggered the regulatory response, but the market's own response to that event was to accelerate the repayment of bank facilities. The transmission mechanism that regulators are stress-testing is one that the market has already substantially shut down.

Where did the risk go?

If $13.2 billion in new debt replaced $0.5 billion in net bank revolver reductions, then approximately $12.7 billion in incremental private credit risk now sits with CLO tranche investors, unsecured bond holders, insurance companies, and pension funds. The risk did not disappear. It migrated from bank balance sheets, where it was supervised, capitalised, and subject to borrowing base discipline, to capital markets structures where it is dispersed, less visible, and not subject to automatic de-leveraging.

That migration matters because the borrowing base was the disciplining mechanism when portfolio risks increase. For example, when a loan converts to payment-in-kind, it stops generating cash interest. Bank revolvers respond to this automatically: PIK loans typically receive lower advance rates or become ineligible collateral, shrinking the available borrowing base and forcing paydowns even without the bank taking discretionary action. The JPMorgan software markdown was the discretionary version of this mechanism. But the routine, formula-driven version operates continuously and is probably larger in aggregate.

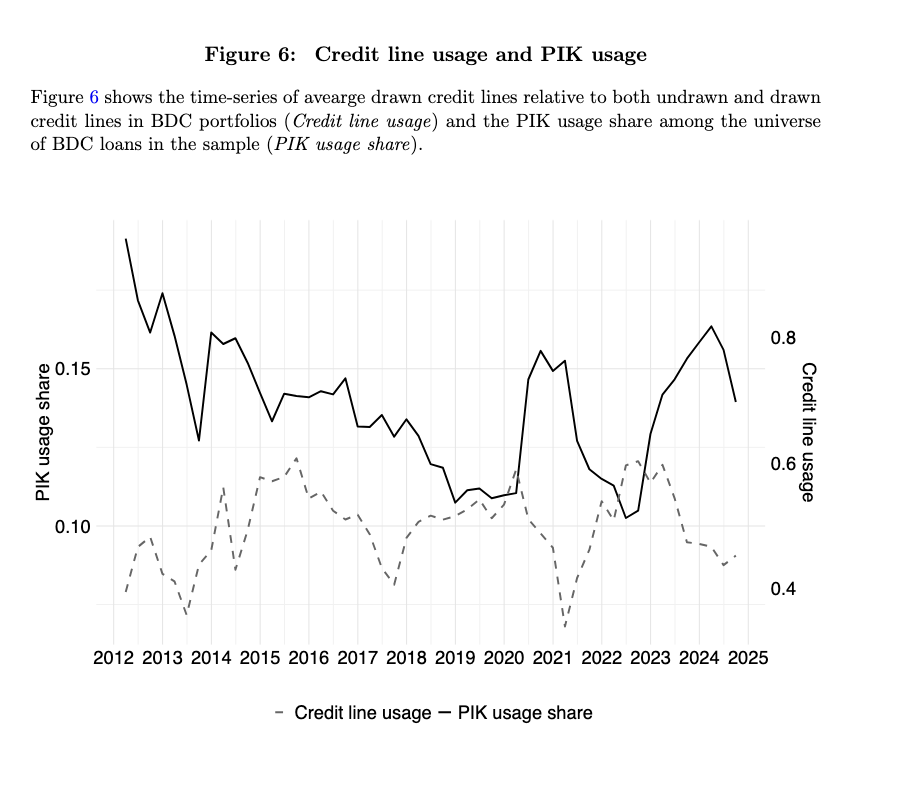

My research with Paul Rintamäki (paper is available here) shows that conversion PIK, existing cash-paying loans switched to PIK mid-contract under distress, predicts significantly worse credit outcomes and leads to maturity extensions rather than restructurings. The dollar amount of PIK in BDC portfolios reached $62.8 billion at Q4 2025, more than double the level at Q4 2022. The value-weighted PIK usage share stood at 12.72%, though this partly reflects compositional effects as large loans entered the denominator. Figure 6, from our BDC sample, shows the relationship between credit line usage and PIK usage over the full 2012–2025 period.

Source: Rintamaki and Steffen (2026)

The pattern is clear. As PIK usage rises, credit line usage falls, not because banks are pulling lines, but because the borrowing base formula mechanically reduces available capacity as portfolios shift from cash-paying to PIK. Banks are being repaid through a de-leveraging mechanism embedded in the contracts themselves. The "bank contagion" that regulators fear is being prevented by the very contractual infrastructure they are now investigating.

But CLOs do not have borrowing bases. Unsecured bonds do not have advance rates. When the same PIK or redemption-prone loan sits in a CLO tranche rather than a bank-financed warehouse, the automatic discipline disappears. The CLO structure holds its collateral to maturity or until the manager decides to trade, there is no formula-driven forced de-leveraging. The liability restructuring documented in the funding waterfall table solves the BDCs' liquidity problem but removes the market discipline that bank revolvers imposed.

What regulators should do instead

The current supervisory architecture is asking the wrong question. The question is not whether banks are exposed to private credit. They are less exposed today than they were six months ago, and the contractual mechanics ensure they will be further de-risked as PIK usage and redemptions continue to rise. The question is who now holds the $13 billion in capital markets instruments that replaced the bank debt, and whether those holders understand the credit risk embedded in the underlying portfolios.

Three data collection priorities follow. First, CLO tranche ownership: which insurance companies, pension funds, and asset managers hold the mezzanine and equity tranches of BDC-originated CLOs? This is where the first losses will materialise if the software "maturity wall" produces defaults at the rates Morgan Stanley (8%) and UBS (14–15% severe case) project. Second, unsecured BDC bond holdings: these are corporate bonds of entities whose portfolios are increasingly dominated by PIK loans and AI-disrupted software exposures. Traditional fixed income investors may hold these without fully appreciating the underlying credit concentration. Third, the interaction between PIK usage and portfolio valuation: current supervisory data captures stated NAVs, but not the conversion PIK rate, the PIK-adjusted interest coverage ratio, or the gap between internal valuation marks and secondary market prices.

The banks are fine and the supervisors checking their books will likely confirm this. The problem is that the risks have moved further into corners of the financial system where nobody is looking.

This is the next in a series of posts on private credit (stress). You can find other posts on my website here.