The Funding Chain Paradox: European Banks, Private Credit, and the Backstop That Depends on What It Replaces

I recently presented new research to the European Systemic Risk Board's Advisory Scientific Committee on a question that has been bothering me for some time: what do we actually know about European bank exposure to private credit?

The short answer is: not enough. And that should concern us, not because the sky is falling, but because a $2 trillion market funded in large part by the global banking system deserves better infrastructure than we currently have.

This post summarizes the key themes from the presentation, which draws on two papers: one with Elisavet Mistopoulou on the funding structure of U.S. Business Development Companies, and one with Franz Hinzen, Giorgio Mondini, and Paul Rintamäki on the cyclicality of direct lending.

Private credit is a countercyclical backstop — and that is good news

The first thing the data show clearly is that private credit does not simply grow alongside syndicated loan markets. It grows instead of them, at precisely the moments when syndicated markets contract. When banks tighten lending standards — as measured by the Fed's Senior Loan Officer Opinion Survey — firms switch from syndicated loans to private credit. The effect is economically large, supply-driven, and concentrated among PE-sponsored borrowers.

This is a stabilizing feature for the real economy. Firms that would otherwise lose access to credit during a tightening cycle can turn to direct lenders. The academic literature has been debating whether private credit complements or substitutes for bank lending. Our evidence suggests the answer depends on the cycle: during normal times the two markets coexist; during stress, private credit absorbs displaced demand.

This substitution pattern aligns with what several other researchers have documented — that BDCs causally expanded into markets vacated by banks after regulatory shocks, and that the growth of private credit is at least partly driven by banks retreating from middle-market lending under capital and liquidity pressure.

The plumbing is more complex than most people realize

Here is where it gets interesting and where the data infrastructure falls short.

We hand-collected facility-level funding data from 195 U.S. BDC filings spanning nine fiscal years (2017–2025). What emerges is not a simple story of "BDCs borrow from banks and lend to companies." It is a multi-tier liability structure comprising revolving credit facilities, SPV warehouse lines, CLO securitizations, and unsecured notes — each with different counterparties, different maturities, and different risk profiles.

The aggregate numbers are striking: $267 billion in total debt outstanding and $353 billion in committed funding as of 2025.

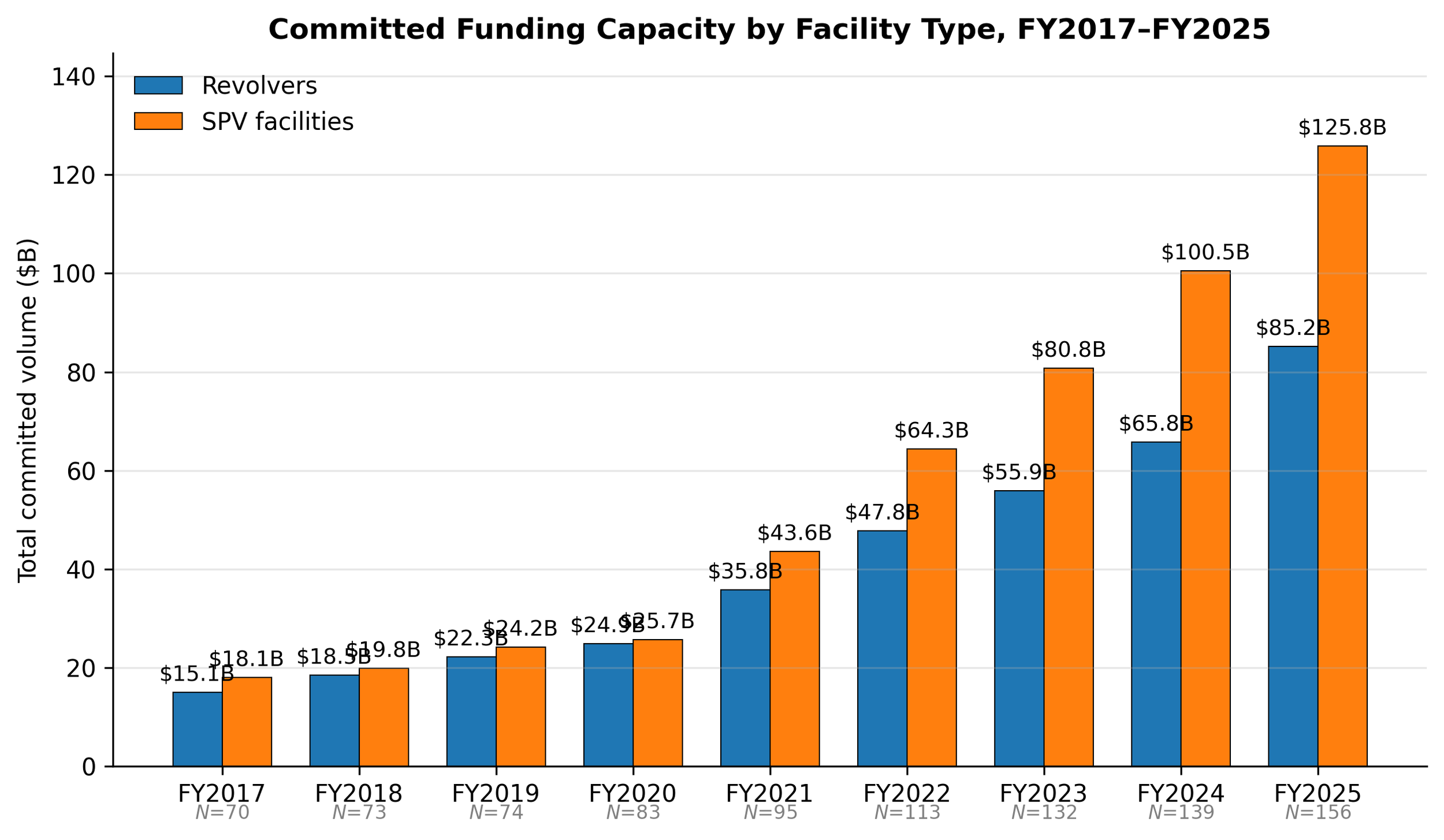

Figure 1. Bank-intermediated funding

Bank-intermediated funding has grown 7x in under a decade. Revolvers and SPV warehouse facilities — the two facility types provided by banks — grew from $33B to $211B in committed capacity between 2017 and 2025. SPV growth, where European banks are most prominent, accounts for the bulk of the increase.

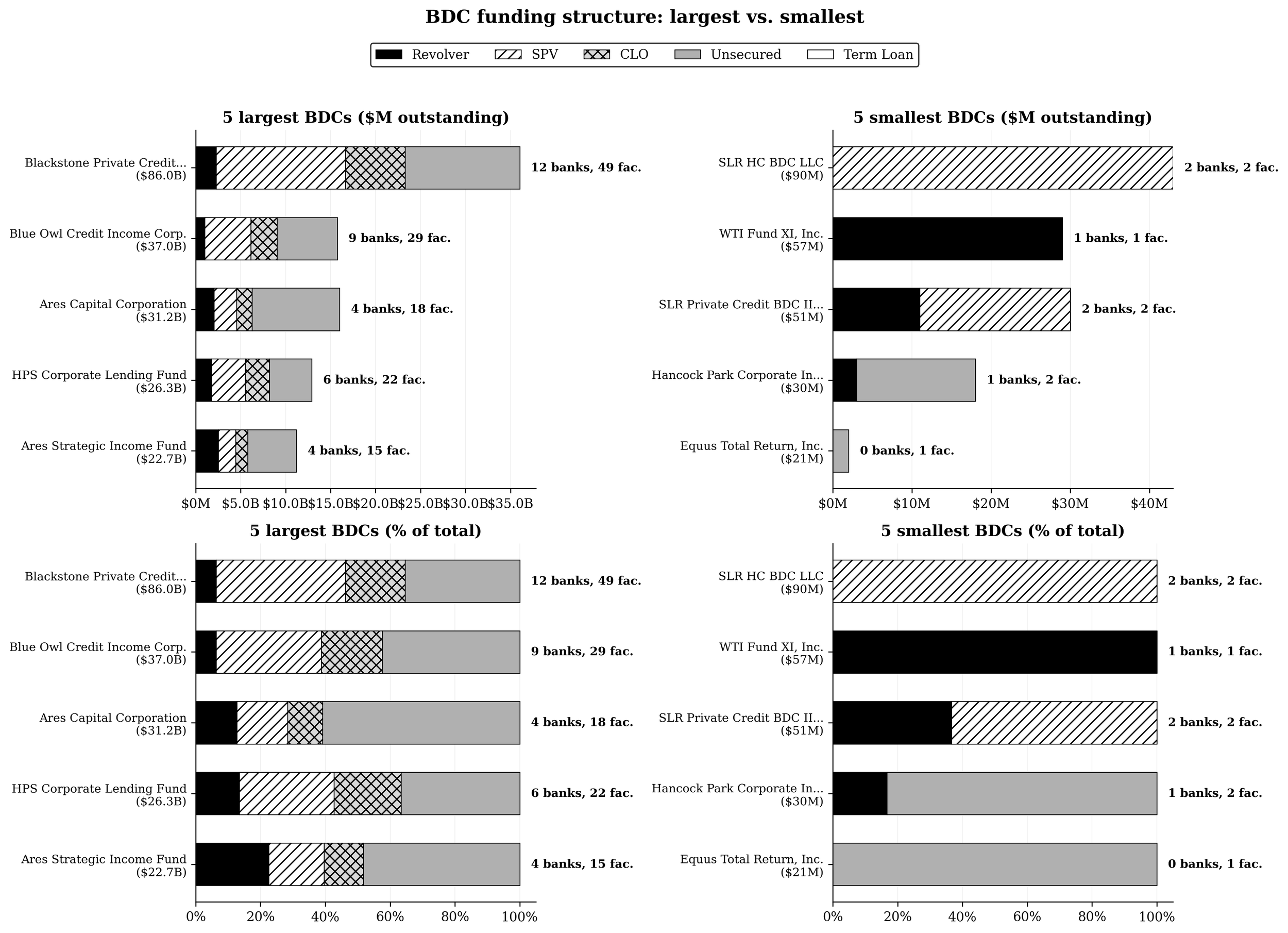

But the aggregates mask substantial heterogeneity. The smallest BDCs are entirely bank-dependent, a single revolving credit line from one or two banks, with no access to capital markets. The largest BDCs have diversified across unsecured bonds, CLO issuance, and multiple bank facilities. The median private (non-traded) BDC has zero unsecured market access.

Figure 2. BDC Funding Structure — Largest vs. Smallest BDCs

No supervisor currently has a consolidated, facility-level view of these exposures. The FSB flagged this as a significant data gap in its May 2026 report on private credit vulnerabilities. The OFR has noted that even supervisory data (Form Y-14) systematically misses SPV-level borrowings because the SPV obligor names cannot be linked back to parent BDCs. Our 10-K-based approach resolves precisely this identification challenge.

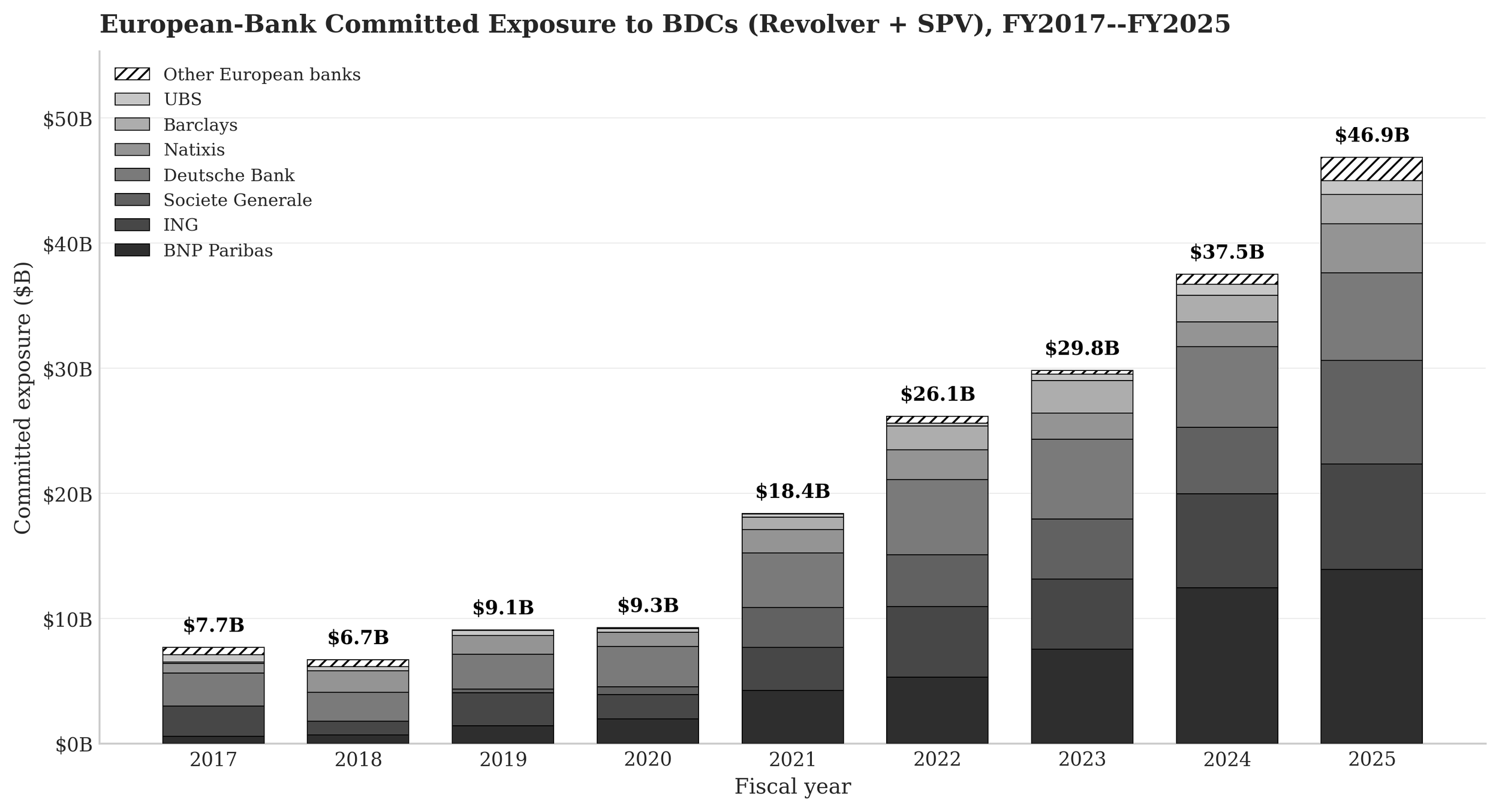

European banks are deeper in than you might think

One of the findings that generated the most discussion at the ESRB was the European dimension. When you look at who actually provides funding to BDCs at the facility level, European banks show up prominently — particularly in SPV warehouse facilities, which are secured against BDC loan portfolios.

The exposure is not trivial. Several European G-SIBs have multi-billion-dollar committed positions. And it is concentrated: the same banks that provide BDC credit lines also hold leveraged loans, warehouse CLOs, and run prime brokerage operations. The risk is not in any single exposure but in the correlation across exposures within the same institutions.

Figure 3. European-Bank Committed Exposure to BDCs, 2017–2025

This matters for European supervisors because these exposures are cross-border (European banks funding U.S.-domiciled vehicles), which means they may not be fully captured in EU stress testing frameworks. SREP processes may miss the concentration.

The paradox at the center

Here is the tension I wanted the committee to sit with:

The countercyclical backstop function — private credit expanding when syndicated markets contract — is genuinely valuable for the real economy. But that backstop is itself funded by the banking system. The same banks that tighten syndicated lending provide the credit lines that fund the BDCs absorbing displaced demand.

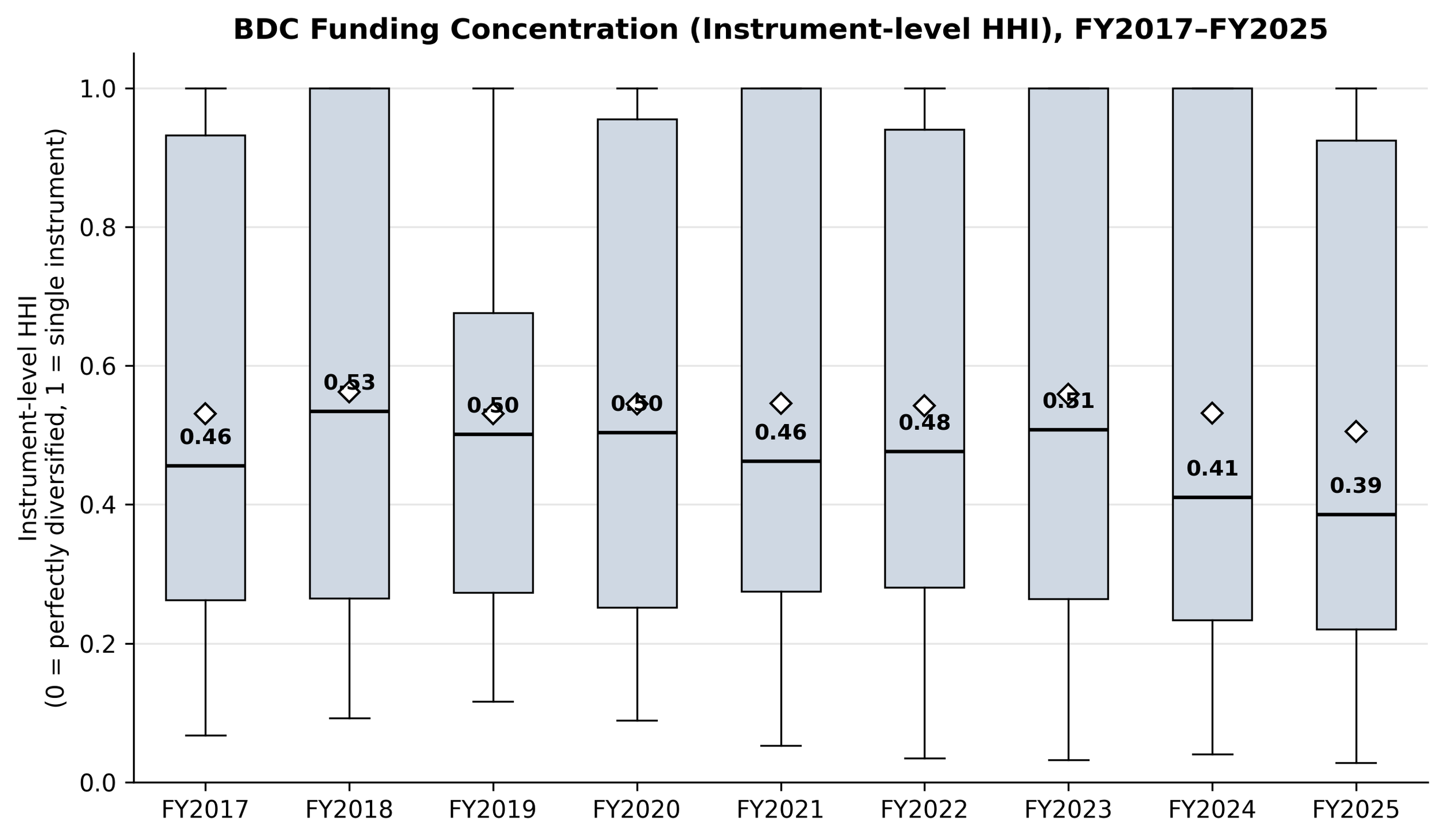

Under stress, this creates a paradox. The backstop function requires BDCs to increase lending precisely when banks are pulling back. To do so, BDCs draw down on their credit facilities — deepening bank exposure at the worst possible time. Bank funding of private credit is procyclical even as private credit lending is countercyclical. Whether this paradox is merely theoretical or operationally binding depends on the structure of BDC funding: how concentrated it is, how short-dated it is, and whether banks can — or will — withdraw. Our data speaks to all three dimensions, and the picture is not uniformly reassuring.

Figure 4. BDC Funding Concentration (Instrument-level HHI), 2017–2025

Not systemic today — but the structure warrants monitoring

I want to be clear: I do not think European bank exposure to private credit is a systemic risk today. Aggregate exposure is small relative to total bank assets, banks are substantially better capitalized than before the financial crisis, and SPV facilities include borrowing-base protections that provide first-loss cushions.

But three dynamics could change the calculus. First, the market is still growing rapidly — SPV commitments alone have grown more than sevenfold over our sample period. Second, regulatory (or subpervisory) arbitrage under Basel III may accelerate the shift from direct lending to funding nonbank lenders, maintaining the same underlying exposure with less capital held against it. Third, the data gaps mean that supervisors may not see concentration building until it becomes a problem.

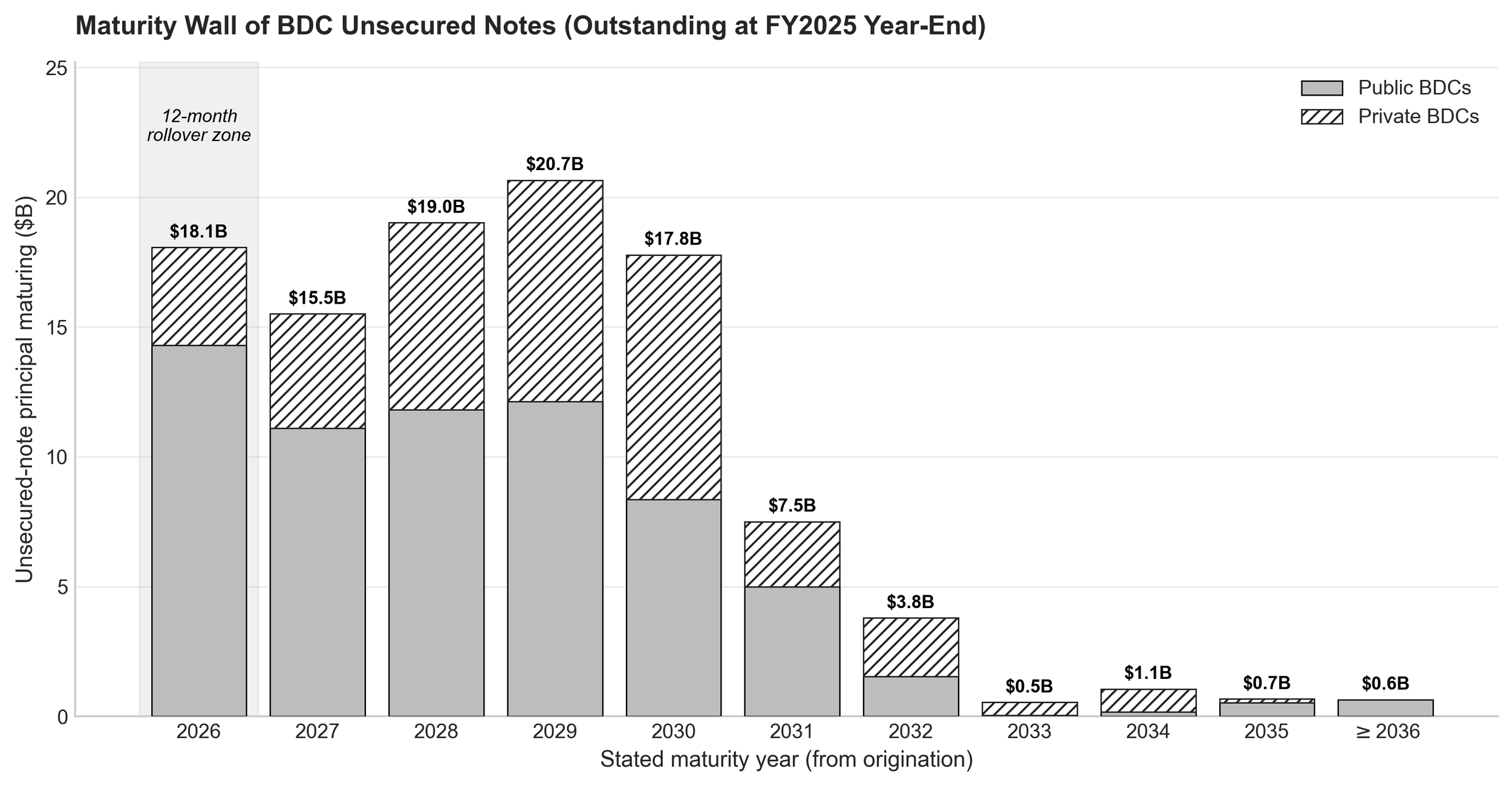

Figure 5. Maturity Wall of BDC Unsecured Notes (Outstanding at FY2025 Year-End)

The question is not whether BNP Paribas can absorb a loss on its BDC book. It is what happens when BDC exposure, leveraged loan holdings, CLO warehousing, and prime brokerage positions all deteriorate together — because they are all linked to the same underlying credit cycle.

What should regulators do?

Five things came up in the discussion that I think are worth highlighting:

Facility-level reporting of bank commitments to private credit vehicles would allow supervisors to track concentration and maturity profiles — something that currently requires hand-collection from public filings.

The cross-border dimension needs attention: European bank exposure to U.S. BDCs is not captured in EU stress tests at the granularity needed.

Maturity structure matters: knowing that a significant share of private BDC revolvers matures within twelve months is operationally important if you want to understand whether the backstop will be available during the next downturn.

Concentration within G-SIBs deserves dedicated monitoring — the same five or six banks appear across every dimension of private credit intermediation.

And finally — and this is perhaps the most important point — tightening capital requirements on private credit exposures too aggressively could inadvertently destroy the countercyclical function that benefits the real economy. The goal should be transparency and monitoring, not restriction.

The bottom line

Private credit has grown from a niche asset class to a $2 trillion market in under a decade. The funding architecture has grown with it. None of this is alarming on its own. But as the market matures, the data infrastructure should mature with it. Facility-level transparency on cross-border bank exposures, maturity profiles, and concentration is not a response to stress — it is what a market of this size warrants as standard practice.

The central tension remains: the countercyclical backstop function that benefits the real economy is itself funded by the banking system. Understanding that funding chain — its structure, its cross-border dimension, its maturity profile — is important precisely because we want it to keep working.

Papers

Mistopoulou & Steffen (2026), "The Funding Structure of Direct Lenders"

Hinzen, Mondini, Rintamäki & Steffen (2026), "The Cyclicality of Direct Lending

Sascha Steffen is the DWS Senior Chair in Finance and Professor of Finance at the Frankfurt School of Finance & Management, and Director of the Centre for European Transformation (CfET).