Why we migt not expect an interest rate increase in the Eurozone soon

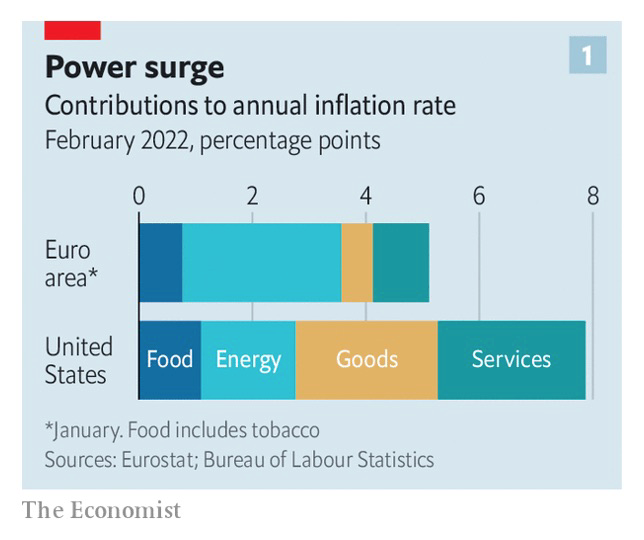

The response of the Fed and ECB to the Ukraine conflict and the associated sanctions and economic consequences. The Fed has forcefully communicated that inflation is too high and problematic, requiring several rate hikes over the course of 2022. In contrast, the ECB has acknowledged higher inflation in the euro area, but has (only) announced a reduction of the QE purchases that have been restarted following the COVID outbreak in 2020. It appears as if the monetary policy in the US and Europe diverges (similar to what we have observed following the global financial crisis). The following figure, taken from the Economist, provides a possible explanation.

Source: Economist March 2022

Looking at this analysis, it appears that not only the percentage differences in realized inflation matter, but also compositional differences. In the US, the contribution of food, goods and services to inflation by far outweigh the contribution of energy. In the euro area, energy costs are driving the inflation rate.

In other words, the increase in inflation appears to be demand driven in the US, due to an improving economy, higher spending and investments. In the euro area, in contrast, rising energy costs, i.e. supply, are the main driver of inflation. A possible interpretation is that economic development has not improved post-COVID to the same degree as in the US. A different monetary policy response might therefore be justified. I.e., an increase in interest rates in the US to address demand related changes in inflation, which - at this time - might not help but rather suppress economic development in the euro area.

I hope this is interesting and please reach out if you have thoughts or questions.