Valuation of Leveraged Loans - Implications for Private Credit

That is a somewhat scary figure as the market tells us risks need to be priced in!

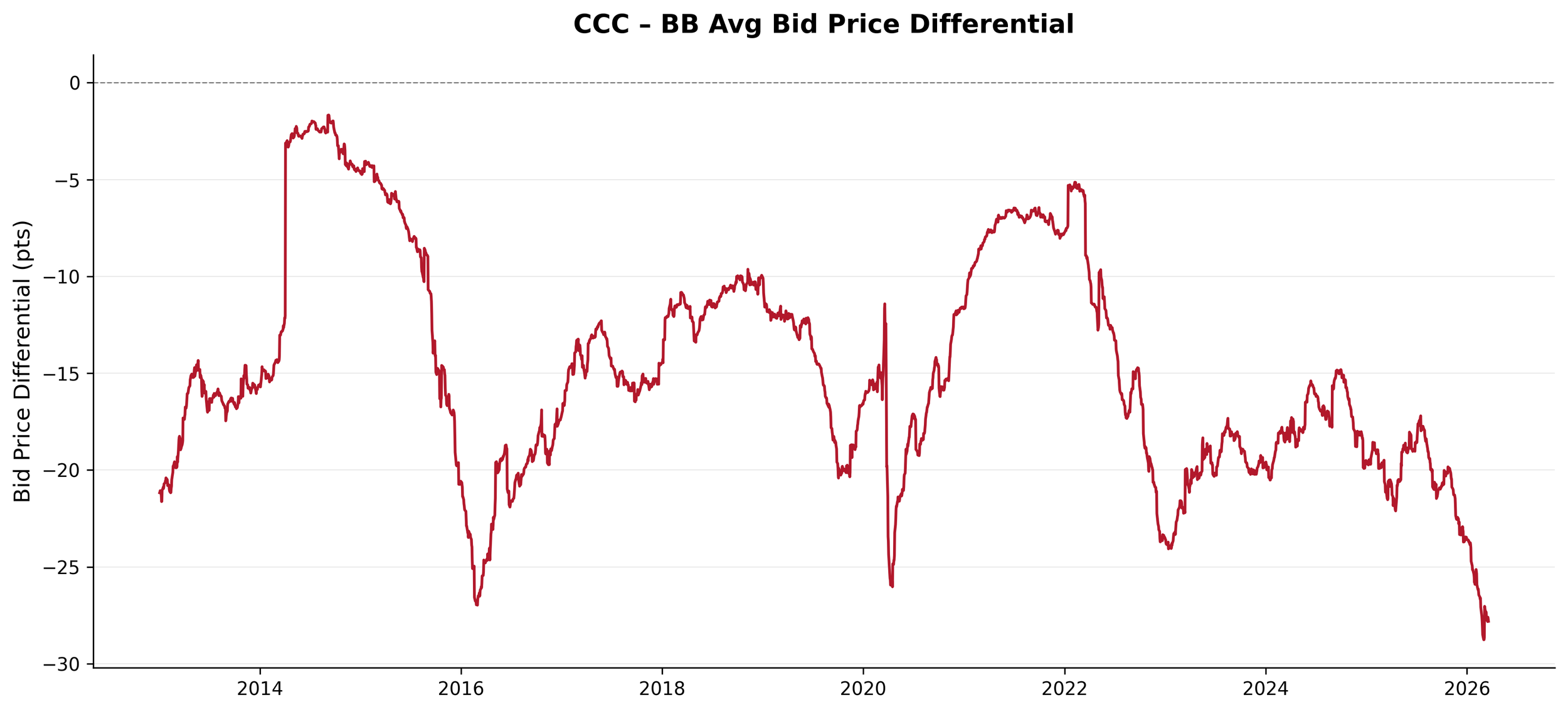

Bid price differential of CCC - BB leveraged loans

Among the riskier loans the best (BB) minus the worst (CCC)

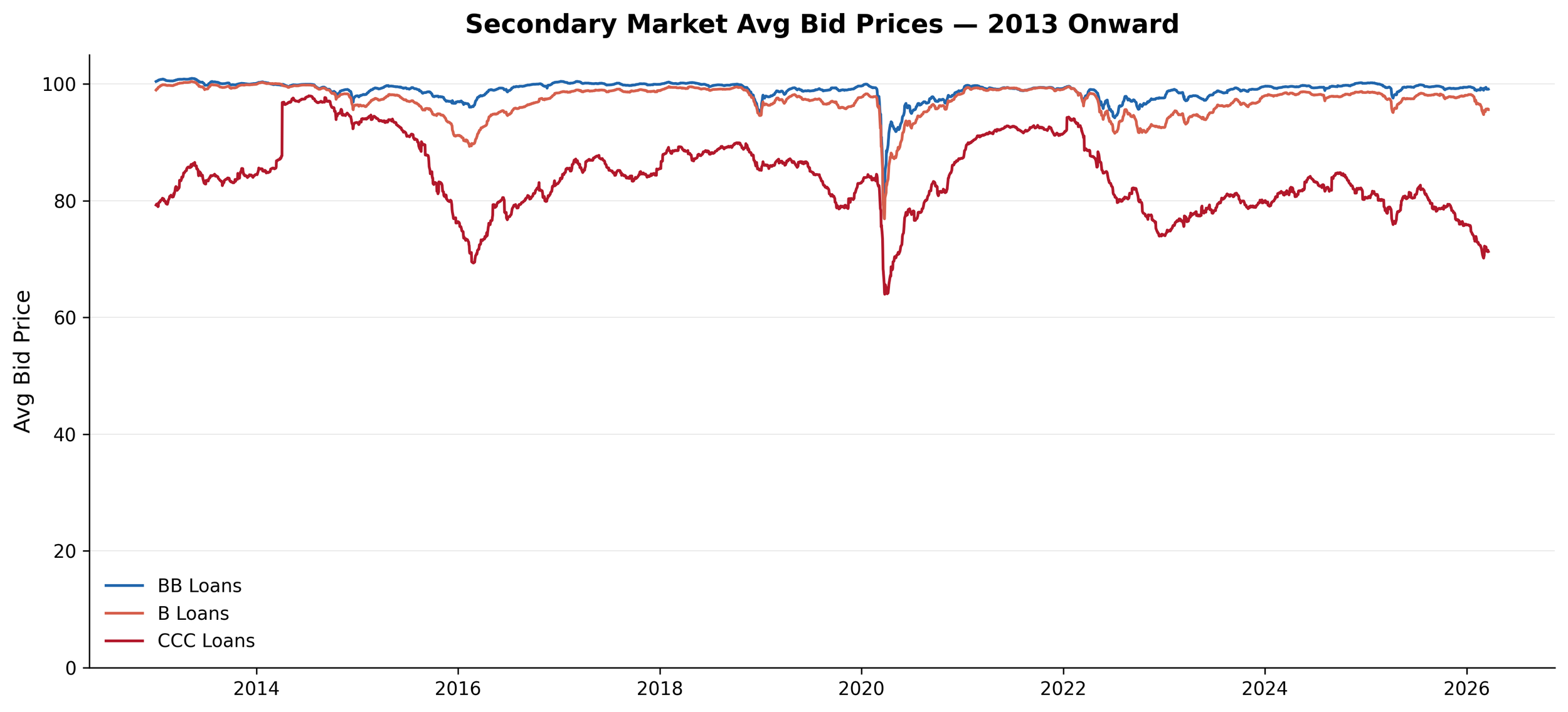

Bid price itself

For all BB-, B-, and CCC-rated US leveraged loans

The price of CCC-rated loans declines while the other rating categories (BB and B) remain somewhat stable. And the price differential is worse than during COVID - and we don't even have a big macro shock (yet).

This does not tell uns what the underlying drivers are, but here are two conjectures:

There is likely some selling pressure of Collateralized Loan Obligations (#CLOs) who have restrictions as to their holdings of CCC rated loans, a selling pressure that easily spills over to other parts of the CLO portfolio (see one of my papers on "fragile financing")

CCC-rated loans is not a big segment of the leveraged loan market (a little bit less than USD 90bn in the US right now of the USD 1.5 tn market). This has declined over time because some of the risk has migrated to private credit. But this has implications for some part of the direct lending portfolios of private credit lenders (not to all, though) and to possible valuation differences people are worried about, when lenders are not yet devaluing according to actual market prices.

One in the pro-column for people worried that actual default rates as of now are likely understated!!

#PrivateCredit

#LeveragedLoans