Bankruptcy of First Brands Group, LLC

In a recent Financial Times article, Jim Chanos warns that the private credit boom is structurally fragile, built on opaque financing and unrealistic return promises, and that First Brands’ bankruptcy may foreshadow broader systemic risks similar to Enron and the subprime crisis.

Some evidence why this is a highly complex case:

High balance-sheet leverage (syndicated in the US and Europe) with roughly USD 5bn in debt and senior secured lenders eventually pushing the firm into bankruptcy. Most exposures in CLOs in the US and Europe

US private credit and CLOs via syndicated loans contributed roughly USD 4 billion in financing (among those 13 BDC lenders with roughly USD 250mn (only) exposure (as of June 2025 and BDC Collateral data)

Weak EBITDA covenants provided a wrong image about liquidity

Most important: > USD 4bn off-balance-sheet financing through SPVs and factoring and supply-financing (pushing also other firms close to bankruptcy).

Collateral pledged multiple times for different layers of debt

UBS appears to be one of the most exposed lenders overall (through off-balance-sheet finance

Figure 1. Secondary Market Price of First Brands LLC (Source: BDC Collateral)

Secondary market prices in Figure 1 shows significant decline in market prices prior to major ratings downgrades highlighting price discovery in loan markets (lots of research about this) and trading of institutional investors (CLOs) out of the distressed debt ahead of time (new research with Paulina Verhoff (Frankfurt School of Finance & Management) and Tony Saunders (NYU Stern School of Business) on this related to trading before covenant violations (coming soon!!).

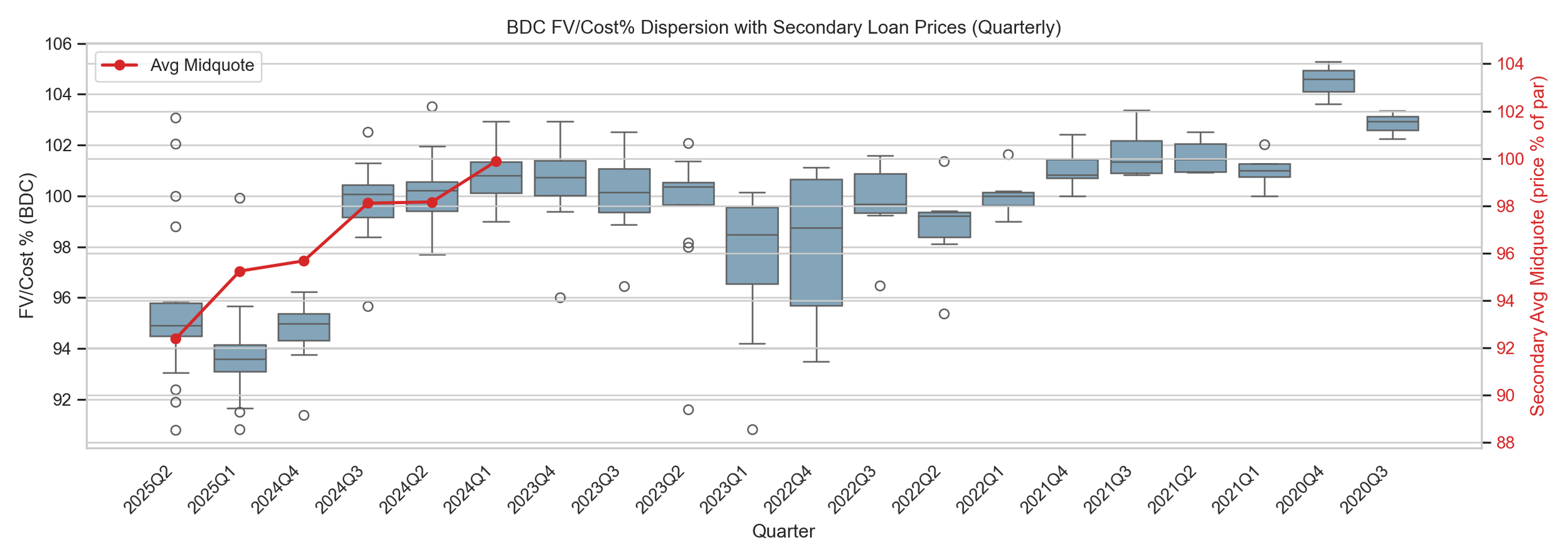

Figure 2. Valuation Dispersion

Figure 2 shows the quarterly dispersion of valuations of BDCs of First Brands’ loans and the secondary loan market mid-quote of traded syndicated loans (red). Valuations dropped already in Q4 2024 when the firm initiated a USD 6bn refinancing (that eventually was cancelled).

Valuations of BDCs dropped faster initially compared to syndicated loan quotes suggestions information about borrower distress was earlier incorporated in private debt valuations. Interesting the high dispersion in the valuation of lenders in Q2 2025, before First Brands defaulted.

More research to come about this!! What other risks are hiding in an opaque industry, flooded with cash and problems to deploy it (sensibly)?

Thoughts about this? Comment below 👇

#research #distress #bankruptcy #privatecredit #complexdebt #loans #pricediscovery #secondarymarkets